Ah, balloon payments. What a friendly-sounding name…

Is it a fitting name, or should we call it ‘bomb payments’ instead? Let’s find out.

In this post, we’ll explain balloon payments, how and why people use ‘em, and look at the pros and cons.

Let’s get into it.

Balloon payment

Adding a balloon payment helps lower the monthly instalment on a loan. Which makes it very attractive in the short term. But balloon payments can be risky. It’s worth understanding the full effects beforehand.

What is balloon payment?

A balloon payment is a large, final lump-sum payment due at the end of a specific type of loan structure. A loan with a balloon payment is structured with smaller monthly payments followed by a big final payment. Known as a balloon payment.

Sometimes, the small monthly payments only cover interest, and the final payment (the balloon payment) covers the principal (or amount before interest).

What is balloon payment on a car?

In car financing, a balloon payment allows the borrower to pay lower monthly instalments by deferring (or ‘putting off’) a portion of the vehicle’s cost to the end of the loan term.

(In some cases, it can help secure a loan when someone doesn’t have the best credit score for car financing.)

We’ll share a great example of how this works to help explain how balloon payments work. That’s next.

How does a balloon payment work?

Taking out a loan with a balloon payment makes the monthly instalment smaller. Without a balloon payment, the monthly cost goes up. The reason a borrower pays less with a balloon payment is that they only pay part of the loan amount in monthly instalments. The last part, the balloon payment, is the amount they pay at the end. It’s a lump sum due in full at the end of their agreement with the lender.

For example, in a car financing agreement, the lender may finance around 70% of the car’s value in monthly payments. Then, make the remaining 30% a balloon payment that’s due as a lump sum at the end of the loan term.

Example: If you buy a car for R300,000 with a 30% balloon payment, you’ll only pay off R210,000 through monthly instalments. At the end of the loan term, you’ll owe R90,000 as the balloon payment.

(Remember, the balloon payment is due in full.)

Why would someone finance a car like this?

Because it makes car ownership more affordable upfront. It requires careful planning, though. Having a large payment due at the end can be risky.

📖 Related content:

Advantages and disadvantages of balloon payments

Loans with balloon payments have pros and cons. Lower monthly instalments are the biggest advantage. On the other hand, there’s a risk of not being able to pay the lump-sum balloon payment.

Advantages of balloon payments

- Lower monthly instalments make financing more affordable in the short term.

- The borrower has more expendable income throughout the loan term.

Disadvantages of balloon payments

- There’s a large lump sum payment due at the end, which may need refinancing.

- Interest costs could be higher over the loan period.

- There’s a financial risk if the borrower can’t make the final balloon payment.

Balloon payment applications

Banks and lenders use balloon payments in different types of financing. Vehicle financing is the most popular application, but balloon payments also show up in home loans and business loans.

Car financing: This is the most common use of balloon payments in South Africa. It lets the buyer reduce the monthly car instalments significantly. But of course, at the end of the loan, they have to either pay the balloon amount, refinance, or trade in the car for a different model.

Home loans: Sometimes, balloon payments are used in home loans. This can reduce monthly bond repayments, but it requires VERY careful financial planning because of the size of the final lump sum payment at the end. Most people end up refinancing the home loan at the end of the term.

Business loans: Businesses can also use balloon payments, and some use them to finance large purchases. Things like equipment, property or other assets. The balloon payment structure keeps monthly expenses lower during the growth phase. With the expectation that the business will have more resources to cover the balloon payment later.

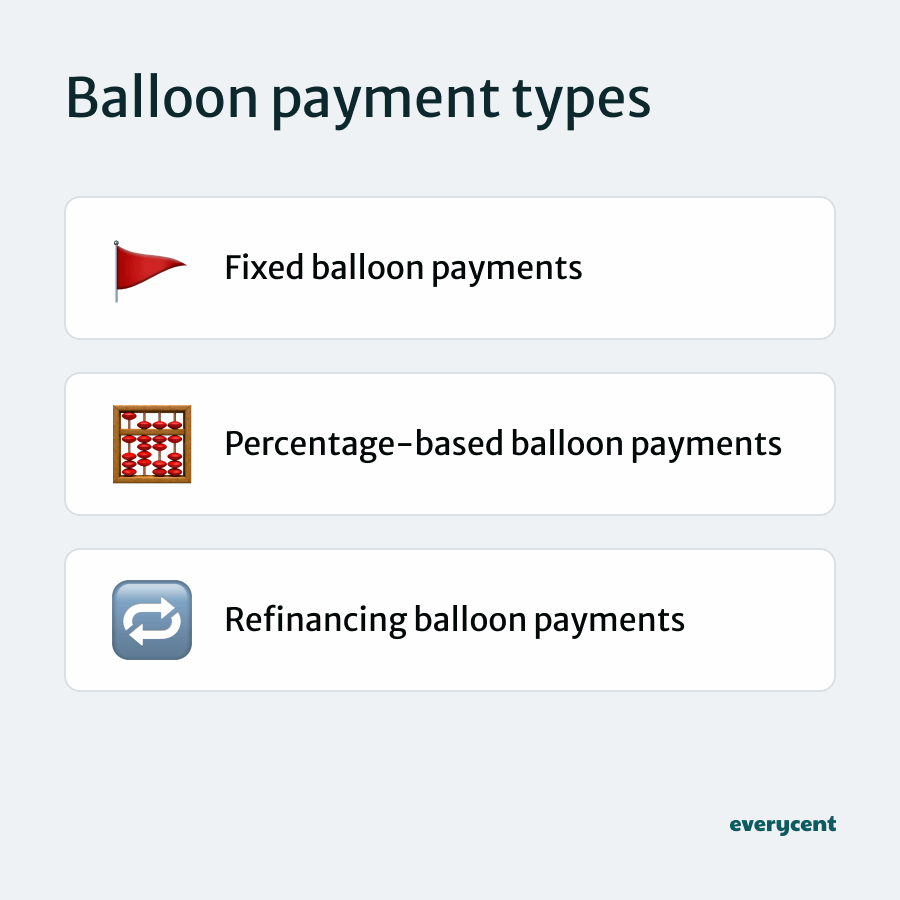

Balloon payment types

There are three different types of balloon payment structures, fixed, percentage-based, and refinancing balloon payments.

Balloon payment types:

- Fixed balloon payment

- Percentage-based balloon payment

- Refinancing balloon payment

Fixed balloon payments use a set balloon amount that doesn’t change over time.

Percentage-based balloon payments use a percentage of the asset’s value, often between 30% and 40%, as the balloon payment.

Refinancing balloon payments allows borrowers to refinance the lump sum at the end of the loan or trade in the asset to cover the payment.

Okay great.

That’s where balloon payments apply and how the different types can be structured.

Still have questions? Good. We’ll address those next.

Frequently asked questions

Does the settlement amount include the balloon payment?

Yes, the balloon payment is usually included in the settlement amount. When settling a loan, the total owed covers the remaining principal and the balloon payment.

Can a balloon payment be refinanced?

Yes, lenders typically allow refinancing of the balloon payment. Borrowers can take out a new loan to cover the lump sum and spread the payments over a new term. Just remember, refinancing typically means the borrower pays more interest overall. Which increases the total cost of the loan.

What happens if the balloon payment can’t be paid?

If a borrower can’t pay the balloon payment, then they can refinance, sell the car or asset, or trade in the vehicle. Some lenders may offer a grace period, but this depends on the lender’s policy. It’s worth re-reading the finance agreement or talking to someone at the company to find out about all the options.

📖 Related content:

Is interest charged on the balloon payment?

Yes, lenders charge interest on the entire loan amount, including the balloon payment. This is important. Interest builds up throughout the loan term, even though the balloon payment is due at the end. This means borrowers may pay more in interest compared to a traditional loan without a balloon structure.

Can the balloon payment be paid off early?

Yes, borrowers can pay off the balloon payment early. Many lenders allow early settlement, which can reduce the total interest cost for the borrower. Early settlement fees may apply.

In summary

Adding a balloon payment can help reduce monthly costs, but it’s important to plan for the large payment at the end. Which can cause a bit of trouble without proper planning.

Thankfully, there are options like refinancing or trade-in.

Think about it carefully. Is the lower repayment worth the risk? And what is the likelihood that you’ll be able to cover the balloon payment at the end?

Sometimes, paying more upfront or buying something more affordable are better options. Choose wisely.

Keep reading on Everycent to learn more about money and finances in South Africa.