You’ve probably been dreaming about it for years, haven’t you?

Getting a new car.

Now, you’re ready. There’s just one last thing to do.

Get approved for car financing (or an auto loan).

Whether your dreams come true (or not) all comes down to your credit score.

So, naturally, you want to find out—what is the credit score required to buy a car in South Africa?

Let’s find out.

What is a credit score?

A credit score is a number (or score) that represents someone’s creditworthiness (how safe it is to lend money to them) based on an analysis of the person’s past credit behaviour.

Lenders, like banks or retail stores, use credit scores to evaluate whether it is safe to lend money to their customers and reduce their chances of losing money from individuals who do not (or cannot) repay their debt.

The lower someone’s credit score, the riskier it may be to lend them money.

Makes sense, right? So, what is the benchmark credit score for car finance in South Africa?

Quick note: some credit bureaus use their own ranges; however, for the sake of this article, we’ll look at the 0 – 999 range used by TransUnion and Experian (two of South Africa’s most prominent credit bureaus.)

Credit score for car finance in South Africa

In South Africa, credit providers generally prefer credit scores above 680. However, a lower score in the range of ~600 may also be approved depending on the specific lender’s criteria and circumstances surrounding the car’s purchase.

Credit scores for car finance:

- Minimum credit score = ~600

- Good credit score = 670 – 749+

Here’s a breakdown.

What is the minimum credit score to buy a car in South Africa?

The minimum credit score required to buy a car in South Africa is typically close to 600; however, the exact score may vary between lenders.

Minimum score: ~600

Keep in mind: If your score hovers around this range, lenders might see you as a high-risk borrower.

This means that you may face higher interest rates or require a larger down payment. It’s not impossible to buy a car with a score of 600 (or slightly lower), but it’s definitely more challenging.

(The credit score requirements to buy a house in South Africa are similar).

What is a good credit score to buy a car in South Africa?

In South Africa, a good credit score to buy a car falls within the higher end of the credit range used by major credit bureaus in the country, which is between 670 and 749 on the 0 – 999 credit rating model.

Good score: 670+

Keep in mind: The higher your score, the better your chances of approval. Plus, you’ll enjoy more favourable interest rates.

📖 Related content: What is a good credit score in South Africa?

Cool. So, roughly 670+ is good and 600 is the minimum. What if your score is even lower?

Where there’s a will, there’s a way.

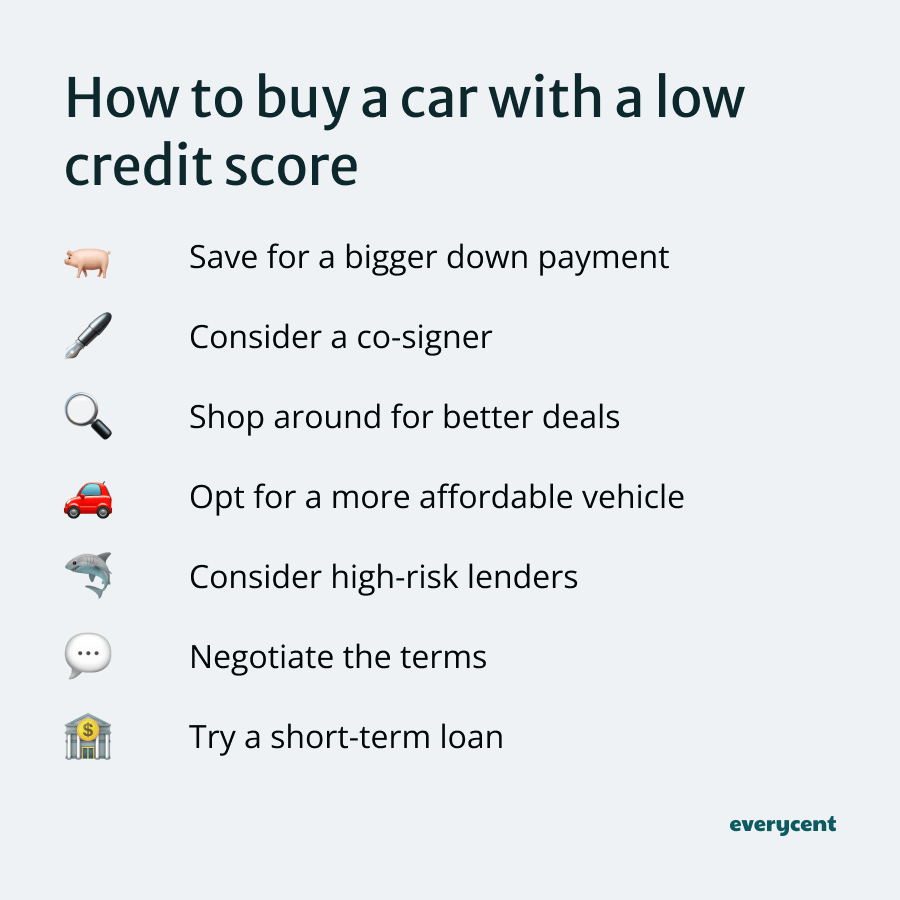

How to buy a car with a low credit score

It’s possible to buy a car with a low credit score; it just requires some extra work or a little assistance.

Here’s how you could do it.

Ways to buy a car with a low credit score:

- Save for a bigger down payment

- Consider a co-signer

- Shop around for better deals

- Opt for a more affordable vehicle

- Consider high-risk lenders

- Negotiate the terms

- Use a short-term loan instead of car financing

- Build your credit score first

Remember, each of these strategies comes with its own set of pros and cons.

It’s essential to thoroughly evaluate your financial situation, consider the total cost of ownership of the vehicle (including loan repayments, insurance, maintenance, and fuel), and make an informed decision.

Save for a bigger down payment

The more money you can put down upfront, the less you have to borrow.

This reduces the lender’s risk, which might help offset the impact of a low credit score.

So, take some more time and save a little extra. A larger down payment can also lead to lower monthly repayments and possibly a lower interest rate. Win-win.

Consider a co-signer

Do you have a family member or a trusted friend with a good credit score?

They can co-sign the car loan with you.

In this case, their creditworthiness reassures lenders and improves your chances of approval.

It’s a big ask, though. As a co-signer, your family member/friend will be equally responsible for repaying the loan if you default.

(If you can’t make the payments, and they can’t help, then the lenders could initiate the vehicle repossession procedure and take away the car.)

Shop around for better deals

Don’t just settle for the first financing option you find.

Different lenders have different criteria for creditworthiness. Credit unions, online lenders, and specialised car finance companies sometimes offer more lenient terms compared to traditional banks, especially for those with lower credit scores.

Opt for a more affordable vehicle

Buying a more affordable car requires less financing, which could improve your chances of getting approved (despite a low credit score). Consider buying a demo car or a used car if necessary. Adding a balloon payment could also help with affordability.

Even if temporary, lower monthly repayments can give you time to work on your credit score to get the dream car next time ‘round.

Consider high-risk lenders

(Not a recommendation. But an option)

Some lenders specialise in “subprime” borrowers — those with low credit scores.

These loans typically come with higher interest rates and fees that reflect the extra risk the lender is taking.

It’s not the ideal option, but it can be a pathway to car ownership when other doors are closed.

Negotiate the terms

Sometimes, a little negotiation is all it takes. Just because you have a low credit score doesn’t mean you can’t negotiate the terms of your car loan.

Don’t hesitate to negotiate the loan terms and the price of the vehicle—being open to harsher terms may get a lender to approve your loan.

Use a short-term loan instead of car financing

If you can afford it, taking a short-term loan (even at a higher interest rate) and paying it back diligently can improve your chances of getting approved and improve your credit score after the fact (if you repay the loan as agreed.)

Then, you could look at refinancing the loan at a better interest rate later on.

Build your credit score first

If you can, take the time to improve your credit score before buying a car. A better credit score will improve your chances of getting approved, plus reduce the overall cost of the loan since you’ll get better interest rates on the loan.

We’ll go over how you can boost your score next.

(Bonus: There’s one more option, which is learning how to make passive income to help pay for the car.)

How to improve your credit score before buying a car

To improve your credit score before buying a car in South Africa, do the following.

How to improve your credit score:

- Check your credit report

- Pay bills on time

- Reduce debt levels

- Avoid new hard inquiries

- Dispute inaccuracies

- Keep old accounts open

By the way, you could check out our post, How to build a good credit score in South Africa, for seven steps that anyone can follow to improve their credit score in South Africa.

Now, here is an explanation of each of the tips we mentioned earlier.

Check your credit report: Access your free credit report from South African bureaus and correct any errors.

Pay bills on time: Prioritise punctual payments for all bills to positively impact your credit score.

Reduce debt levels: Reduce your debt load and aim for a credit utilisation rate under 30%.

Avoid new hard inquiries: Avoid unnecessary new credit applications before seeking car finance.

Dispute inaccuracies: Dispute any discrepancies on your credit report with the respective bureau.

Keep old accounts open: Keep longstanding accounts open to demonstrate a stable credit history.

Sometimes, our credit scores get hurt because there’s too much debt, and it is hard to keep up. If that’s the case, it may be worthwhile to talk to a debt counsellor and apply for debt counselling.

Debt counselling is a great way to make debt more affordable and make it easier to make monthly repayments more consistently (+ there are other cool benefits of debt counselling).

Debt counselling (or debt review) can help you get on your feet first. Then, you can apply for credit after debt review.

If everything is under control, focus on some of the other tips instead.

In summary

Whether your score is low, good, or excellent, there’s always a pathway to that dream car.

If you have a lower score, remember:

- There are alternative strategies; and

- You can always improve your score over time.

For those with good or excellent scores—congrats! You’re good to go.

Want to learn more? Keep reading on Everycent.