A good credit score can turn a dream into a reality.

And do so at a lower cost.

Want to buy a home? A car? Pay to study?

A loan is all you need, and a good credit score is the only thing standing between most South Africans and realising that dream.

But how do you build a good credit score and improve your credit record to make it happen?

Let’s find out.

How to build a good credit score in South Africa

Before we reveal the secrets that’ll help you to boost your credit score, let’s go over the fundamentals.

A quick credit score 101, if you will.

What is a credit report?

A credit report is a detailed record of an individual’s credit history. It is a comprehensive document (or digital record nowadays) that details past credit behaviour, including loans, credit cards, credit utilisation, late payments, defaults, and more.

You could think of it as a financial report card compiled by credit bureaus that lenders, renters, or employers may use to evaluate creditworthiness or financial reliability.

It contains everything.

Personal information, credit accounts, credit inquiries, and public records or collections provide a snapshot of financial behaviour and obligations.

Now, let’s talk about the credit score itself.

What is a credit score?

A credit score is a numerical representation of someone’s creditworthiness (how safe it is to lend money to them) which typically ranges from 0 – 999.

The higher the score, the better. A good credit score shows lenders how consistent someone is at repaying the money they borrow. It helps lenders decide whether someone can get a loan or credit card, how much it will cost, and what the terms should be to reduce their risk as the lender.

What’s a good credit score in South Africa?

In South Africa, a good credit score is 670 or higher. Credit scores range from 0 to 999, with most scores around 300 to 850. A score above 670 is considered good and indicates responsible borrowing, use of credit, reliable repayment and stable financial management.

Scores below 580 are considered bad (hard to get a loan), while scores between 580 and 670 are seen as fair (loans may be more expensive). Then, scores above 670 are typically seen as very good, while those in the 800-999 range are considered excellent, offering the best conditions and interest rates.

We should all strive for higher scores within this range to maximise our financial opportunities and save some money with better terms.

As a side note, you may also enjoy these two articles:

- What is a good credit score to buy a house in South Africa?

- Credit score required to buy car in South Africa

How to build your credit score in South Africa

Building a good credit score isn’t an overnight process, but with consistent effort and financial discipline, it’s certainly achievable.

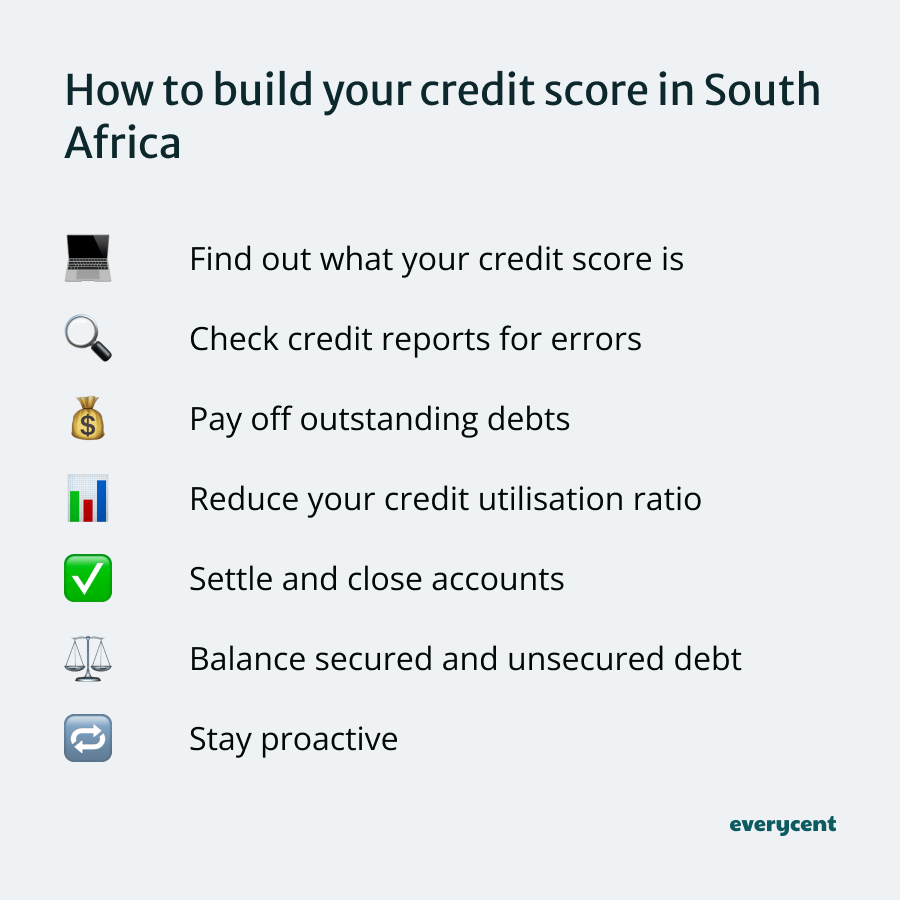

Follow these 7 steps to improve your credit score:

- Find out what your credit score is

- Check credit reports for errors

- Pay off outstanding debts (overdue accounts and arrears)

- Reduce your credit utilisation ratio to below 30%

- Settle and close accounts

- Balance secured and unsecured debt

- Stay proactive

Find out what your credit score is

The first step in building a good credit score is to know where you stand.

Many South Africans don’t know their credit score, and you can’t fix a problem that you don’t understand.

So, the first thing you should do is check your credit score.

The easiest way to find out what your credit score is is to check an online platform like ClearScore or My Credit Check.

These are online platforms that let anyone check their credit score in South Africa for free.

If you want a more comprehensive credit report, then you could get one from one of SA’s credit bureaus like Experian or TransUnion. Typically, you get one free comprehensive report per year.

Okay, once you’ve got your report, it’s on to step two.

📖 Bonus reading: How to check if you are ‘blacklisted’ in South Africa

Check credit reports for errors

Mistakes happen, so it’s not impossible for you to have errors on your credit report.

The wrong error could be hurting your credit score.

Make a habit of regularly reviewing your credit reports so you can spot and fix mistakes.

It could be incorrectly listed late payment or incorrect account details — identify and dispute any errors with the credit bureau so you can maintain a healthy credit score.

Pay off outstanding debts (overdue accounts and arrears)

Late payments and defaulted accounts can really hurt your credit score.

One of the most effective ways to boost your credit score is by paying off any outstanding debts.

This includes overdue accounts and arrears.

Clearing these debts demonstrates financial responsibility and trustworthiness — a positive signal — which can improve your credit score.

Anyone who is struggling to keep up with their debt could consider applying for debt counselling. It may make it easier to repay outstanding debts by reducing the monthly debt instalment.

Here are two articles on debt counselling:

Reduce your credit utilisation ratio to below 30%

Maintaining a balanced use of credit shows that you’re not dependent on your debt. Therefore, keeping the ratio of credit available to you that you use in the range of 30% is good for your credit score.

It’s a sign of responsible credit management and financial stability — again, positive signals.

By maintaining a lower ratio, you enhance your creditworthiness and improve your chances of getting favourable credit terms. Some finance professionals recommend staying close to 30% rather than using too little, like 5%.

What is a credit utilisation ratio?

Your credit utilisation ratio is the percentage of your total available credit that you’re using.

For instance, if you have a credit card limit of R10,000 and you’ve used R3,000, your credit utilisation ratio is 30%.

How to lower your credit utilisation ratio

To lower your credit utilisation ratio, you can either reduce your outstanding balances or request a higher credit limit while not increasing your spending.

Settle and close accounts

Paying off and closing accounts, especially those with outstanding balances, can positively impact your credit score. Settling debts shows lenders that you’re responsible with credit.

When you close an account, ensure it’s properly documented as ‘paid in full’ or ‘settled’.

📖 Related content: How to clear your credit record

Note on credit history length and when to keep an older account open

When you settle and close accounts, it can positively affect your credit score. However, it’s important to note that the length of your credit history also plays a role in your score.

Sometimes, keeping an older account open, especially if it has a positive history, can be beneficial.

This shows lenders a longer track record of responsible credit management.

Balance secured and unsecured debt

Balancing secured and unsecured debt is an important aspect of building a robust credit profile.

What is secured vs unsecured debt?

Secured debt is tied to an asset, like a home loan secured against your house. Unsecured debt, like credit cards, isn’t backed by any asset.

To balance these, diversify your credit portfolio by responsibly managing a mix of both types. This balance demonstrates to lenders that you can handle various types of credit and still repay responsibly.

Maintain a healthy balance and pay on time on both secured and unsecured debt accounts.

Stay proactive

Regularly take proactive steps to build and maintain your credit score.

Do the following to build your credit score proactively:

- Repay instalments on time

- Limit requests for new credit

- Monitor your credit report

Repay instalments on time: Lenders want to see that you repay your debt and do it on time. Always pay on time and pay your outstanding balance in full.

Limit requests for new credit: Too many credit applications could indicate a dependence on credit. Try not to apply for new loans, accounts, or credit cards too often.

Monitor your credit report: Regularly check your credit report for any errors or discrepancies and make sure that what you’re doing is working.

It may take a little time, so be patient, but over time, you should start to see improvements.

In Summary

Building a good credit score in South Africa is about consistent financial discipline and smart credit management.

Think about it this way. If you asked yourself, “Would a bank or lender see this behaviour as a sign of responsible credit management?” would the answer be yes or no?

If the answer is yes, then the action will likely improve your credit score.

Start applying these principles and building your credit score today — it’ll make it easier to achieve your financial goals.

Bonus: If you need a little extra cash to get it done, try preparing some of these cheap dinner ideas to save some extra money.

Want to learn more? Keep reading on Everycent.