Every South African knows several people who have undergone debt counselling or are still in the process (they just don’t know that they do).

Debt counsellors are the ones who help these over-indebted South Africans go from being in the red (bad finances) to being in the clear (debt freedom).

There’s a lot more to it, though. So let’s get started.

What is a debt counsellor?

A debt counsellor is a financial professional who helps individuals struggling with debt resolve their debt problems by providing debt management services and assistance.

Since the National Credit Act (NCA) introduced debt counselling in South Africa in 2007, debt counsellors have been working under the regulation of the National Credit Regulator (NCR) to help individuals restore their finances and become debt-free.

📚 Debt counsellor definition

A professional who provides debt management and resolution services.

Basically, the one to call when something has to be done about debt that is getting out of control.

For example, when you get a Section 129 letter of demand, then it may be time to turn to a debt counsellor for help. They could save you (or your employer) from being issued with a garnishee order.

That’s neat, but it doesn’t explain what a debt counsellor does. Let’s go over a debt counsellor’s duties and responsibilities.

⭐ Bonus read: What is the difference between debt counselling and debt review?

What does a debt counsellor do?

Here’s the list of everything that a debt counsellor does on a day-to-day basis:

| Assess clients’ financial situations | Collects financial information that relates to income, expenses, and debts to assess an applicant’s financial well-being. |

| Negotiate with creditors | Debt counsellors talk to creditors on behalf of their clients and convince them to restructure their payment terms. This helps to reduce monthly debt repayment totals and, in some cases, even interest rates. |

| Create debt repayment plans | This is a debt counsellor’s superpower. Debt repayment plans reduce the monthly cost of debt and consolidate debt (bring it together). This means consumers only pay one reduced amount each month. |

| Keep records | There’s usually a lot of paperwork involved. Debt counsellors use dedicated software to keep track of payments, the total owed, defaults, and more. No Excel updates and paper punching for the clients – hooray! |

| Monitor client progress | Debt counsellors support their clients, follow up, and prompt them to ensure that they stick to the repayment plan and meet their goal (debt-free status). |

| Represent clients in court | In some cases, debt counsellors will take care of various court proceedings that relate to debt collections and other legal actions—providing legal support and financial expertise. |

| Provide financial education | Debt counsellors can share advice on things like budgeting, saving, credit utilisation, and more. |

That is pretty impressive if you ask us.

Since there is so much to do, and often thousands of South Africans are being helped at the same, most debt counsellors that you’ll encounter online have grown into organisations. Therefore, there’s usually a whole team behind each over-indebted individual.

⭐ Bonus read: Advantages and disadvantages of debt counselling.

The NCR and regulation that protect consumers

Alright, what does the NCR have to do with debt counsellors?

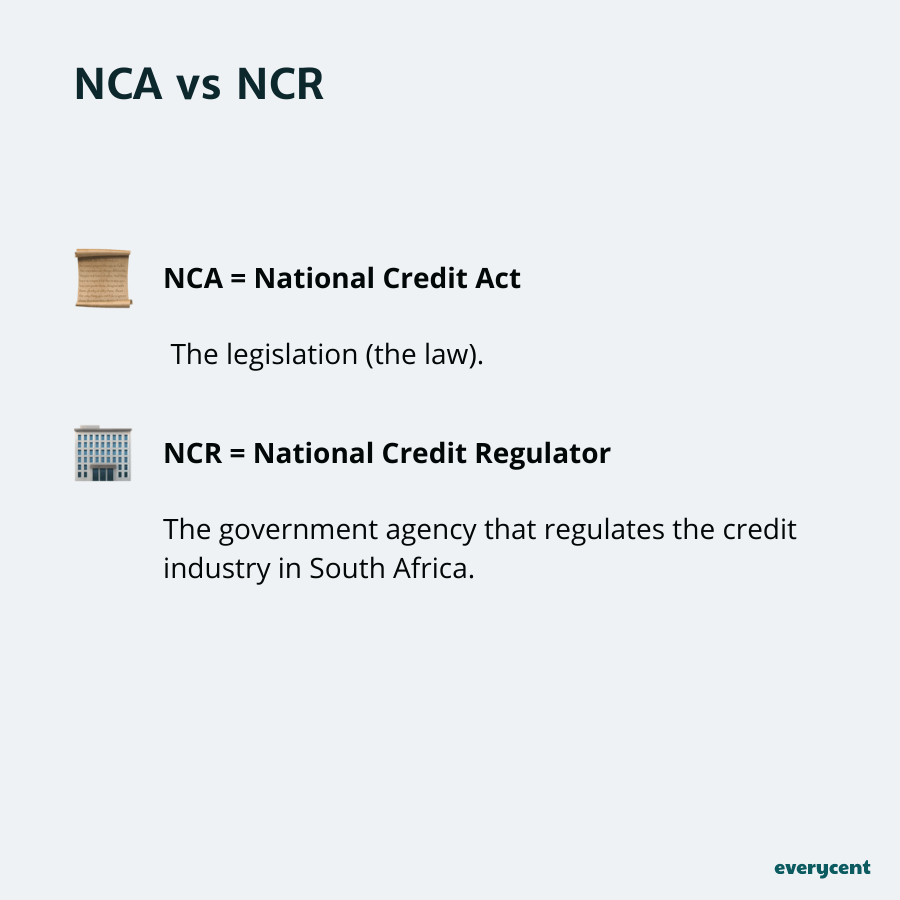

Earlier, we mentioned the National Credit Act (NCA) and the National Credit Regulator (NCR).

Here’s how they relate to debt counsellors and debt counselling:

The National Credit Act = legislation (the law)

The National Credit Regulator = regulatory agency (an organisation that keeps things in check)

Together, the NCA and the NCR make it possible to apply for debt counselling and go through an efficient process (*mostly efficient). The NCA sets the rules, and the NCR enforces them.

The NCR also sets the debt counselling fees.

Think of the NCR as the enforcer that ensures compliance with the NCA and regulates the activities of credit providers, credit bureaus, and debt counsellors (that’s right. The NCR regulates all the big banks like FNB and Capietc, too).

Here is a list of requirements that a debt counsellor has to meet:

- Hold the necessary qualifications and experience

- Adhere to the NCR code of conduct

- Disclose all fees

- Provide clear, accurate, and complete information

- Protect client information and privacy

- Adhere to the proper debt review procedures

- Register with the NCR (and renew their registration annually)

- Submit regular reports to comply with the NCR’s reporting requirements

The NCR makes it safe. Hence, the importance of working with registered debt counsellors.

Another thing to look for is membership in one of South Africa’s debt counselling associations.

Debt counsellors associations

Debt counsellors associations are advocates for consumer-friendly policies and regulations, they promote higher standards, professional development and better training within the industry.

There are a couple of debt counselling associations in South Africa

These are the most recognizable:

- Debt Counsellors Association of South Africa (DCASA)

- National Debt Counsellors Association (NDCA)

- National Debt Mediation Association (NDMA)

- South African Debt Review Industry Association (SADRIA)

The associations serve several functions, such as:

- Helping to regulate the industry

- Offer professional development to debt counsellors

- Advocate for both consumers and debt counsellors

- Act as representatives for the debt counselling industry

It’s surprising how many people are involved. And with good reason. Helping South Africans over-indebted consumers is an important mission. It’s one that everyone wants to get right.

Despite all these superheroes, there are a couple of villains in the space too. People that don’t follow the rules and don’t adhere to the regulations.

On that note, let’s review how to choose a trustworthy DC (short for debt counsellor).

How to choose a registered debt counsellor

The internet is crawling with people who proclaim “debt counselling is a scam”, detailing their awful encounters in lengthy 1-star reviews. But the truth is, not all debt counsellors were created equal. As with any service, some people just aren’t that good, and others might actually be scammers.

Why are we sharing this? To emphasise the importance of choosing a dependable debt counsellor (we recommend only working with NCR-registered debt counsellors).

Here’s a simple three-step framework for picking the right debt counsellor:

- Do some research and compare different debt counsellors (check things like their reputation, awards, and associations.)

- Verify that they’re registered with the National Credit Regulator (NCR) in South Africa – here’s the NCR’s database of registered debt counsellors.

- Ask questions. Curiosity is allowed. Get dependable, straight answers to build confidence before signing up.

Side note: debt counsellors can fall into one of many categories depending on the size of their operation.

Here are the different categories:

- Boutique = 1 debt counsellor with less than 100 clients

- Small debt counsellor = 1 or more debt counsellors with 100 – 300 clients

- Medium debt counsellor = 1 or more debt counsellors with 300 to 1,000 clients

- Large debt counsellor = More than 1 debt counsellor with 1,000+ clients (operating regionally or nationally)

- National debt counselling practice = More than 1 debt counsellor with 4,000+ clients (operating nationally)

Final thoughts

If there’s one thing that stands out after learning more about debt counsellors, it’s that what they’re doing is very important.

Not being able to keep up with debt is a serious problem—one that impacts thousands of individuals and the country’s economy as a whole.

And it is comforting to know that there are teams of people, regulators, and associations, all working together to make it as safe and efficient as possible.

Want to learn more? Keep reading on Everycent.