What now?

You just got a summons for your debt… What’s next?

Well, some pretty serious stuff, actually. A summons for debt is not the kind of thing you can safely ignore.

But, don’t worry. We’ll walk you through what you can do. By the end of this post you’ll have the answer.

Let’s get started.

What to do when you get a summons for debt in South Africa

When you receive a summons for debt in South Africa, you can either pay the debt or dispute the claim by filing a defence. If you ignore the summons, the court may take further legal action. Which could lead to a garnishee order and salary or income deductions or a warrant of execution to repossess assets.

Essentially, you could either:

- Respond and pay the debt.

- Get a lawyer and defend the summons.

Unless you’re going to pay, get a lawyer to help with the defence. It’s all part of a legal process, and things can get tricky without the help.

Not sure, whether you need a lawyer or not?

We’ll cover what to do when you receive a summons for debt in a sec.

First, you need a little background information. Check out the meaning of summons and how the process unfolds.

What is a summons for debt (summons meaning in law)

A summons is a legal document issued by a court. It starts the litigation process and means a case is open. For cases involving debt, it means creditors are initiating legal proceedings as part of the debt collection process.

The summons typically details the amount of debt, the creditor’s claim, and the recipient’s obligation to respond.

If you get one… take it very seriously.

Not responding or ignoring a summons leads to more serious legal action.

Summons procedure

The summons process starts when the creditor’s attorney prepares the summons document. Then, a sheriff of the court has to personally deliver it to the debtor. The summons includes important details like the case number, the court’s location, and the deadline for a response—usually within 10 days.

Here is a step-by-step breakdown.

Steps in the summons process for debt in South Africa:

- Demand and notice: Before the summons, the creditor sends a Letter of Demand or a Section 129 notice (as per the National Credit Act). If the notice goes unanswered, then it’s on to step 2.

- Drafting and approval of the summons: If you don’t settle the debt, the creditor’s lawyer writes up a summons. The court checks and approves it. They’ll note the debt amount and legal reasons for the claim and give it a case number.

- Service of the summons: The court’s sheriff delivers the summons to you in person to make sure you know about it. And make it legally binding.

- Response to the summons: You have 10 days to prepare and send your answer to the court or the creditor’s lawyer.

- Court proceedings and judgement: If unresolved through pre-trial efforts, both parties attend a court hearing where the case is presented. In the court hearing, the court looks at evidence and arguments to decide whether the defending party is innocent or guilty and issues a judgement.

- Enforcement of judgement: If the judgement favours the creditor, enforcement actions will follow. This could be wage garnishment, asset seizure, or bank account attachment. Anything helps the creditor or debt collector recover the debt.

📖 Related content:

Here’s an example…

Sam misses several payments. Gets a Section 129 Letter of Demand, and doesn’t respond. But then, Sam receives a summons. The sheriff delivers the summons to her home, handing it to her personally. Now, Sam has to talk to a lawyer. Who reviews her financial situation and summons details.

Scenario 1: Sam goes to court to defend the claim (the goal may be to reduce the amount or dismiss the case.)

Scenario 2: Sam negotiates a manageable payment plan, reduced settlement or pays to satisfy the requirements of the case. Note, it’s best to have this formalised in court to prevent further legal issues.

Now, what if you’re in Sam’s shoes?

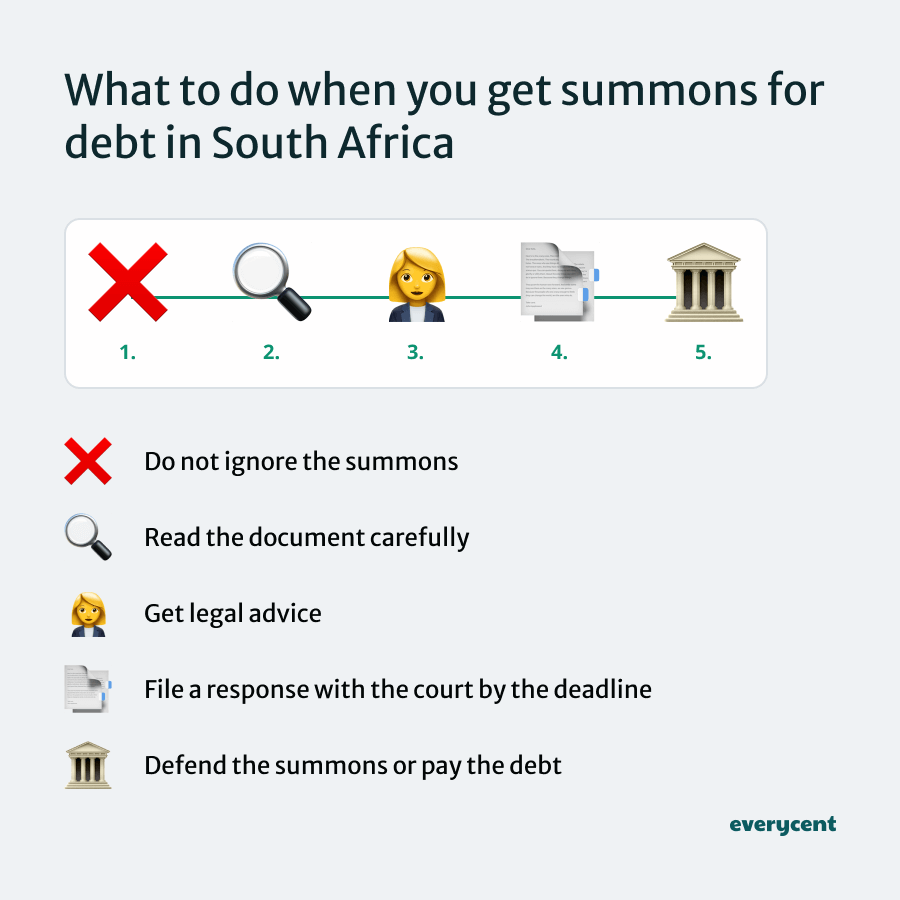

What to do when you receive a summons for debt

When you get a summons for debt, don’t ignore it. Start by reading it carefully and checking if everything is accurate. You’ll need to file a response with the court by the deadline. You can either negotiate to reach a settlement with the creditors or defend the case.

Here’s a step-by-step look at your options:

- Do not ignore the summons: If you ignore the summons the court could rule against you without hearing your side (known as a default judgement). The outcome could mean that creditors get to take your belongings or your money to recover the debt.

- Read the document carefully: Make sure you understand the claim and check whether everything is accurate.

- Get legal advice (if possible): It is advisable to talk to a legal professional who specialises in debt issues. They can help formulate a response and handle most of the legal work.

- Respond: You may decide to either settle the debt outside of court (if possible), dispute the claim if there are valid grounds and defend it in court, or negotiate a payment plan. The response must be filed with the court by the deadline.

- Defend or pay: Follow through with your response. This could be by defending the claims in pre-trial efforts or in court. Otherwise, it could mean settling the debt or making payments according to the agreed upon payment plan.

Before we wrap up this post. Check out some of the most frequently asked questions.

Frequently asked questions

How must a summons be served in South Africa?

In South Africa, the court’s sheriff must personally deliver a summons to you. If you’re not available, the sheriff can give the summons to someone over 16 at your home or work. This makes sure you know about the legal action against you.

What information should a summons contain?

A summons for debt in South Africa should include several key pieces of information:

- The full name and address of the court where the case will be heard.

- The parties involved in the case. Including the creditor and debtor.

- The amount of debt claimed.

- The cause of action that led to the debt.

- The period within which you, the debtor, must respond to the summons. Usually ten days from the date of service.

- Details of where and to whom the response should be submitted, typically the court or the attorney representing the creditor.

What happens if you get summoned to court and don’t go?

If you ignore a summons and miss your court date, the court can rule against you without hearing your side. Which can lead to:

- Garnishment of wages: Part of your paycheck could be taken to pay off the debt.

- Seizure of assets: Things like your car or other valuable items might be taken.

As you can tell, it’s not the kind of thing you can safely ignore.

In summary

Getting a summons for debt is serious.

It’s something that requires immediate and careful attention.

Re-read this post to make sure you understand the legal process and know how to respond. (Even if it means paying money you can’t easily afford right now.)

Keep reading on Everycent to learn more about money and finances in South Africa.